People searching for a home buyer checklist aren’t usually confused about what a house is. They’re overwhelmed by how many things have to happen in the right order and how little room there is to get it wrong.

The process has five phases: financial prep, preapproval, house hunting, closing, and moving in. Each one feeds the next. What you do in month one shapes what’s possible in month three.

This guide covers every step in order. Follow it, and you won’t miss anything that matters.

Get Your Finances in Order Before You Start Looking

Your credit score and debt-to-income ratio decide which loans you can get. Know both before you talk to a single lender.

Start with your credit report, not just the score. Read the actual report. Errors show up more than most buyers expect. Disputing one takes 30 to 60 days to fix. That’s two months you don’t have once you’re under contract.

Once you’ve checked for errors, pay down your revolving balances. Your credit utilization rate, which is how much of your available credit you’re using, moves your score faster than almost anything else.

Avoid Opening New Credit Accounts Before Applying

Don’t open any new credit accounts in the 90 days before you apply. One new inquiry can drop your score at the worst possible time. I’ve seen buyers lose a rate tier over a store card opened for a discount three weeks before applying.

Calculate Your Debt-to-Income Ratio Early

Then work out your debt-to-income ratio, or DTI. Divide your total monthly debt payments by your gross monthly income.

If that number is above 43 to 45 percent, most conventional loan programs won’t approve you, no matter how good your credit score is.

FHA loans give you a bit more room, but there’s still a limit. Most buyers find this out at the lender’s desk. Don’t be one of them.

What Documents to Collect

Get these together before your lender asks. Having them ready cuts out a week of back-and-forth that holds up your preapproval.

- W-2s from the last two years

- Federal tax returns from the last two years

- Recent pay stubs for the last 30 days

- Bank statements for all accounts for the last two to three months

- Investment or retirement account statements

- Proof of any extra income: rental income, alimony, or child support

- Government-issued photo ID

Having this list ready tells your lender you’re serious. More importantly, it means you won’t be the one causing delays.

How Much Home Can You Actually Afford?

A lender’s preapproval number and your real budget are not the same thing. Lenders tell you the most they’ll lend. That’s not the most you should spend.

Three things shape what you can really buy: your monthly obligations, how much you’ve saved, and whether any assistance programs can shift the numbers before you lock in a figure.

Run Your Own Numbers First

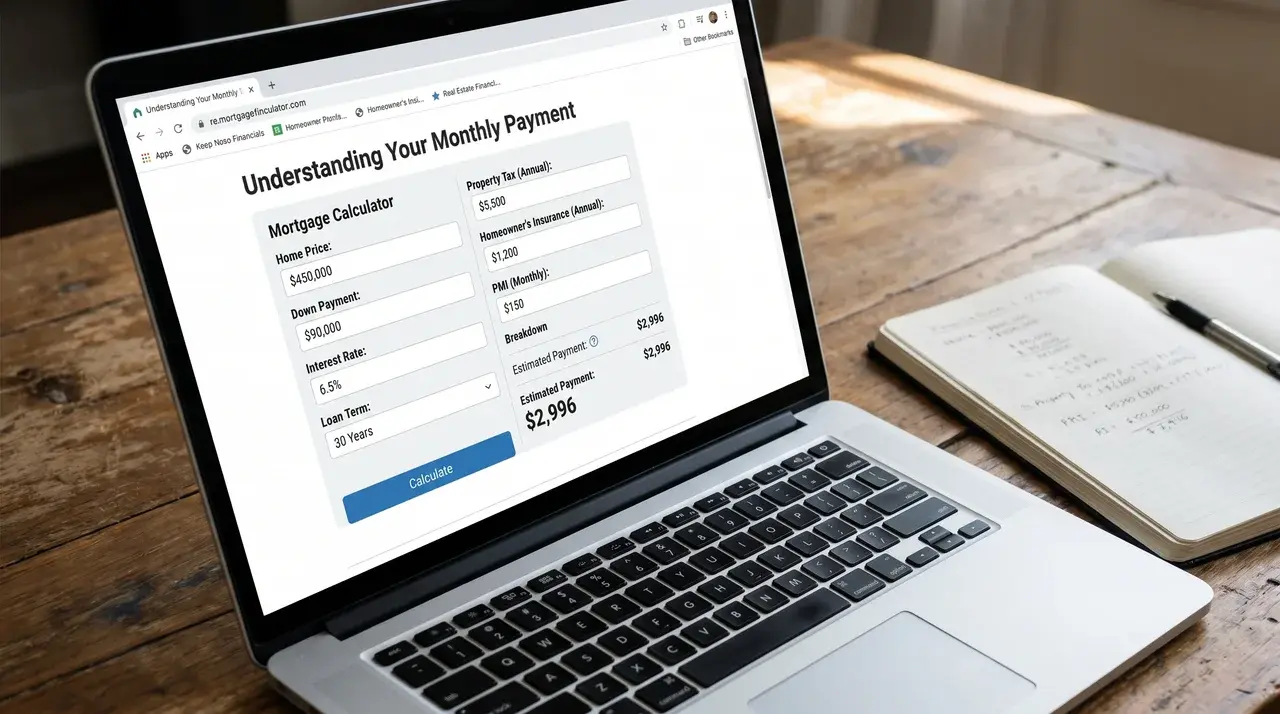

Your monthly payment is more than principal and interest.

Add property taxes, homeowners insurance, and, if your down payment is under 20%, private mortgage insurance, or PMI.

Many online mortgage calculators leave those out. That makes your estimated payment look a lot lower than it will actually be. Run the full number. You’re not being cautious; you’re just being honest with yourself.

Down Payment Assistance Programs

If you think you have to save every dollar of the down payment yourself, you may be wrong. That’s one of the most common mistakes I see first-time buyers make.

Down payment assistance programs exist at the federal, state, and local levels. Some are grants. Some are low-interest second loans.

Eligibility often depends on your income or where the home is located. Look into what’s available in your area before you decide on a down payment amount. Assistance can change what’s within reach.

Down Payment Size and What It Changes

Putting more down isn’t just about a smaller loan. It changes your whole cost picture in ways that add up over years.

PMI kicks in when your down payment is below 20%. It adds to your monthly payment and stays until you hit 20% equity on a conventional loan.

Going from 5% down to 10% can shift which programs you qualify for and cut years off your PMI payments. On a $400,000 home, that gap becomes real money over time.

How to Get Preapproved and Compare Lenders

A preapproval letter proves to sellers that you’re a real buyer. Without one, your offer is just a number on paper.

Here’s the difference that actually matters in practice:

- Prequalification is an estimate based on numbers you report yourself, unverified, and worth very little when competition is tight.

- Preapproval means a lender checked your credit and reviewed your real documents: W-2s, tax returns, pay stubs, bank statements.

Sellers and their agents know the difference the moment they see it.

Get a Loan Estimate From Multiple Lenders

Get a Loan Estimate from at least three lenders before you pick one. It’s a standard document that makes comparing rates and fees easy.

Run all your applications within a 14 to 45 day window. Credit bureaus count multiple mortgage inquiries in that period as one. Shopping with three lenders costs you nothing on your score.

FHA vs. Conventional Loans

Two loan programs cover most first-time buyers. Your credit and savings decide which one fits.

| FHA Loan | Conventional Loan | |

|---|---|---|

| Min. Credit Score | 580 (3.5% down) or 500 (10% down) | 620+ |

| Min. Down Payment | 3.5% | 3% |

| Mortgage Insurance | Upfront fee + monthly charge | PMI only (no upfront fee) |

| Insurance Removed? | Not automatically on older loans | Yes — drops at 20% equity |

| Best For | Lower credit or limited savings | Strong credit and solid savings |

| Long-Term Cost | Higher if you stay in the loan | Usually cheaper over time |

FHA is a tool, not a fallback. If it fits your profile, use it. Just know what you’re paying for.

How to Search for A Home without Losing Your Budget

House hunting without a clear filter is how buyers end up writing offers on homes they love but can’t afford or settling for things they’ll regret. The fix is deciding what you won’t give up before you set foot in a single showing.

Fixed vs. Fixable: What to Decide Before Your First Showing

Every home feature falls into one of two buckets.

- Fixed things are things you can’t change after you buy: location, school district, lot size, floor plan, distance to highways.

- Fixable things are things you can change: paint, floors, fixtures, and an old kitchen.

Write down three to five fixed requirements before you start. Filter every search by those. If a home fails a fixed item, skip the tour. No amount of charm makes up for a commute you hate or a school district you didn’t want.

I have a friend who broke a fixed rule for a house with good bones and has lived with that choice for years. Write the list. Keep it.

Why You Need a Buyer’s Agent

In most deals, your buyer’s agent gets paid from the seller’s proceeds at closing. It doesn’t cost you anything. Skipping representation doesn’t save you money; it just means you negotiate without backup, for free.

A good buyer’s agent pulls comparable sales so you know if the price is fair. They watch contract deadlines so you don’t miss one and lose a contingency. They handle the repair negotiation after inspection. You give up real leverage when you go it alone.

Talk to at least two agents before you choose one. Ask them:

- How many buyers have they helped in the past year?

- How well they know your target area.

Those two questions tell you more than any bio on a website.

How to Make an Offer and Use the Inspection to Protect Yourself

An offer is more than a price. The terms you put in and the ones you leave out decide how protected you are between signing and closing.

1. What Goes Into an Offer

In a hot market, you may feel pushed to waive one. Before you do, make sure you understand exactly what risk you’re taking on.

Earnest Money

It is a good-faith deposit you put down when your offer is accepted. It shows the seller you’re serious and goes toward your closing costs at the end.

Amounts usually run 1 to 3 percent of the purchase price. Ask your agent what’s normal in your market right now.

Contingencies

They are the clauses that protect you if something goes wrong. The three that matter most are the

- inspection contingency

- financing contingency

- Appraisal contingency.

The inspection contingency lets you renegotiate or walk away after the inspection.

The financing contingency protects you if your loan doesn’t come through.

The appraisal contingency protects you if the home is valued below what you agreed to pay without it; you owe the difference.

2. How to Use the Inspection Report

A standard home inspection covers what the inspector can see and reach: electrical, plumbing, HVAC, roof surface, and structure.

It doesn’t find hidden defects behind walls or under floors. it’s just what the job covers. You need to know that going in.

Using the Inspection Report in Negotiations

The report is a negotiation tool. Use it. After the inspection, you can ask the seller for repair credits, a lower price, or specific repairs before closing.

Your agent handles that conversation. If the inspector flags something major, the roof, the HVAC, or the foundation, bring in a specialist before you decide what to do.

The inspection isn’t a pass/fail test. It’s information. What matters is what you do with it.

What Happens at Closing and What to Bring

Closing is a legal and financial event with specific documents and hard deadlines. If you know what to expect, you walk in to review

At least three business days before closing, your lender must send you the Closing Disclosure. It’s the final breakdown of every cost in the deal.

Go through it line by line next to your original Loan Estimate. The numbers should match. If anything changed, it’s something to question before you sign.

Review Your Closing Disclosure Early

Do your final walk-through within 24 to 48 hours before closing.

You’re checking two things: that agreed repairs got done, and that the home looks the same as when you made your offer.

Run the taps. Turn on the heat. Walk every room. If something changed, you still have time to raise it before you own the place.

Complete Your Final Walk-Through

On closing day, bring your photo ID and certified funds a cashier’s check or wire transfer for your down payment and closing costs.

Closing costs usually run 2 to 6 percent of the purchase price, on top of your down payment. Confirm the exact number with your lender the day before. No surprises at the table.

Sign the paperwork, the loan gets funded, and the home is yours. Then you get the keys.

What to Do After You Get the Keys

- Change the locks immediately: Rekey or replace exterior locks on day one. Previous owners, contractors, tenants, or agents may still have copies, so this removes that risk right away.

- Set up utilities before move-in: Transfer water, gas, electricity, and internet into your name by closing day. Contact providers at least a week ahead and confirm activation dates to avoid service gaps.

- Update your address everywhere important: Notify the post office for mail forwarding, but also update your bank, employer, IRS, and DMV directly since sensitive documents should not rely on forwarding alone.

- Do a first-month maintenance check: Locate the main water shutoff, label the circuit breaker if needed, replace HVAC filters, and review your inspection report for anything marked “monitor” so you can track it properly.

Conclusion

Every phase of buying a home builds on the one before it. Your financial work decides which loans you qualify for. Your loan sets your price range.

Your price range decides which offers make sense. That’s what a first-time home buyer checklist is really tracking, not just tasks, but the order they have to happen in.

People who get through this without panic aren’t the lucky ones. They’re the ones who knew what was coming. Now you do too.

Frequently Asked Questions

What credit score do I need to buy a home for the first time?

Most conventional loans need a score of 620 or higher. FHA loans accept scores as low as 580 with 3.5% down, or 500 with 10% down. A higher score gets you a lower interest rate. If you’re below 620, paying down balances and fixing report errors are the fastest ways to move that number before you apply.

How much money do I need saved before buying a home?

On top of your down payment, 3% to 20%, depending on the loan, you need to cover closing costs, moving expenses, and a few months of emergency savings. On a $300,000 home with 5% down, total upfront funds often land between $25,000 and $35,000. Check the current figures with your lender before you commit to a number.

How long does it take to buy a house as a first-time buyer?

From active searching to closing, expect three to six months. Getting your finances ready, saving, fixing credit, and gathering documents can add several months before that. Once a contract is signed, closing takes four to six weeks, depending on the loan type and how fast your lender moves.

Do I need a real estate agent as a first-time buyer?

In most deals, the buyer’s agent gets paid from the seller’s proceeds at closing nothing comes out of your pocket. Buyer’s agents pull comparable sales, manage deadlines, and negotiate on your behalf. Going without representation means giving up experienced help at no cost savings to you.