Most people treat their mortgage as a fixed cost. Money out, every month, nothing back.

House hacking changes that. You buy a property, live in part of it, and rent the rest so tenants help cover what you owe.

Simple idea. But the details matter; the right property, the right loan, the right setup.

Today, I’ll walk you through all of it: what house hacking is, what qualifies, how the money works, and what you’re actually signing up for.

What Is House Hacking?

House hacking means buying a property, living in it as your primary residence, and renting part of it so tenants offset your ownership costs.

The “living there” part isn’t a footnote. It’s what makes the whole thing work.

Because you live in the property, the purchase counts as an owner-occupant transaction, not an investment property buy. That one difference unlocks loan programs that regular real estate investors can’t touch.

- An FHA loan requires as little as 3.5% down.

- A VA loan, for eligible borrowers, requires nothing.

- Standard investment properties usually need 15% to 25% upfront.

I’ve watched first-time buyers miss this completely. They get excited about the rental income and never connect it to why they got the loan they did. The low down payment exists because they’re living there. That’s the part worth understanding.

The moment you move out and rent the whole place, it stops being a primary residence. The financing terms that made the deal possible may no longer apply and your lender likely has occupancy requirements you agreed to at closing.

Property type doesn’t define house hacking. A duplex works. So does a single-family home with a rented spare room. What defines it is owning the property, living in it, and using rent to reduce what ownership costs you.

What Counts as House Hacking?

One rule covers it: you live on the property and earn income from part of it. Both. If that’s true, you’re house hacking.

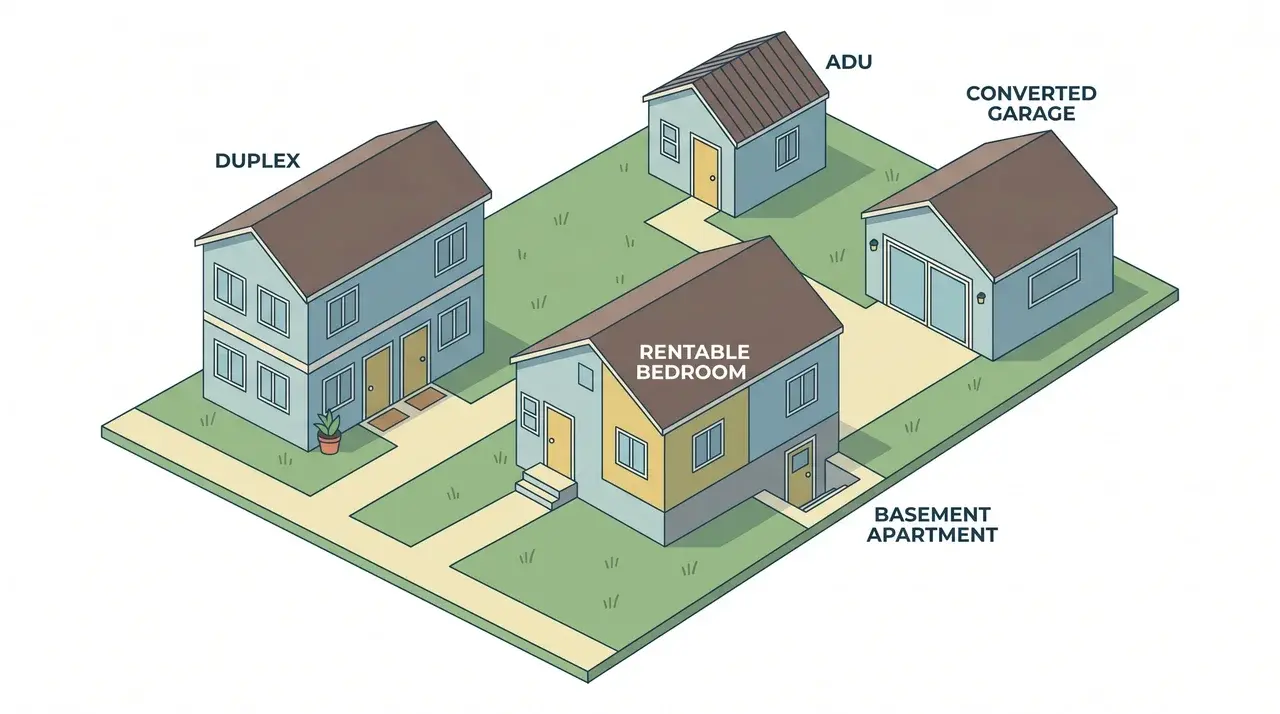

Qualifying setups include a spare bedroom, a finished basement, a separate ADU (a second living unit on the same lot), or a converted garage, while you live in the main home.

Duplexes, triplexes, and fourplexes qualify when you occupy one unit and rent the others. Listing a spare room on Airbnb or Vrbo counts too, as long as you’re living on the property.

What disqualifies a setup is just as clear. If you’re not living there, it’s a rental property. Not a house hack. The table below covers the most common edge cases:

| Qualifies | Does Not Qualify |

|---|---|

| Renting bedrooms | Never living there |

| Renting a basement unit | Moving out and renting all of it |

| Renting an ADU | Subletting while living elsewhere |

| Living in one unit of a duplex/triplex/fourplex | Listing the whole home while away |

Cross into full-property rental territory and lenders treat it differently. Higher down payments. Higher interest rates. The residency rule isn’t just a definition; it’s what makes the strategy financially viable in the first place.

How Does House Hacking Actually Work?

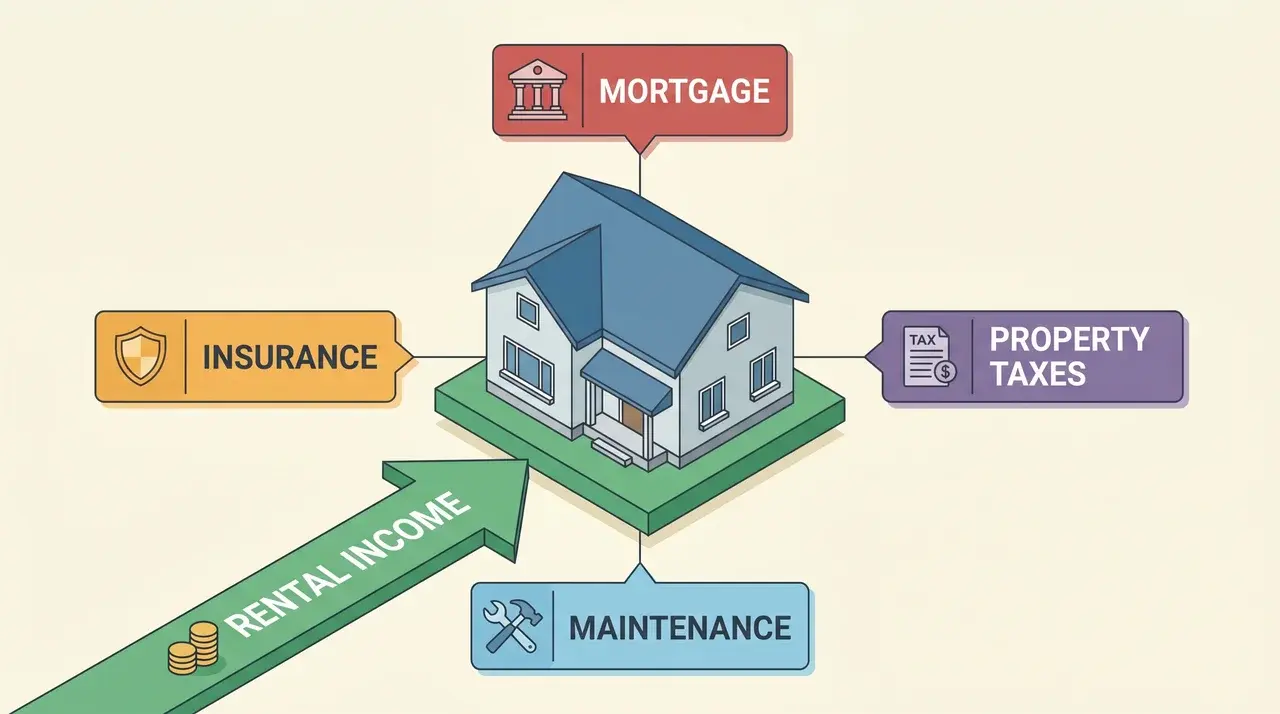

Rent comes in. It goes straight against your monthly ownership cost. That cost includes your loan payment, property taxes, and insurance. Whatever rent covers, you don’t pay out of pocket.

Here’s how each piece of that plays out.

The Equity Side

But the rent doesn’t just lower your bill. Every payment you make on the mortgage, including the part your tenant funded, chips away at your loan balance. You’re building equity. Your tenant is not. They pay you; you keep accumulating ownership in the asset.

If the property goes up in value over time, that’s property appreciation. Your loan balance is falling while the asset value rises. Both forces work in your favor at the same time, and they work whether tenants cover half your payment or all of it.

The Vacancy Risk

Here’s the part I’ve seen hurt people more than anything else: vacancy.

When a tenant leaves, the income stops. But the mortgage doesn’t. You’re back to covering 100% of a payment you may have bought the property expecting not to carry alone.

If your budget only works with a tenant in place, one empty month can put you in real trouble fast. That’s not a scare tactic. It’s the stress test you should run before you buy.

The Maintenance Reality

Experienced investors protect against this by setting aside roughly 1% to 2% of the property’s value each year for maintenance. A water heater, a section of roof, a broken appliance, these come on their own schedule, not yours. The reserve is what keeps one repair from becoming a crisis.

The income side of house hacking is appealing. The strategy holds up when you’ve pressure-tested the expense side just as hard.

The income side of house hacking is appealing. The strategy holds up when you’ve pressure-tested the expense side just as hard.

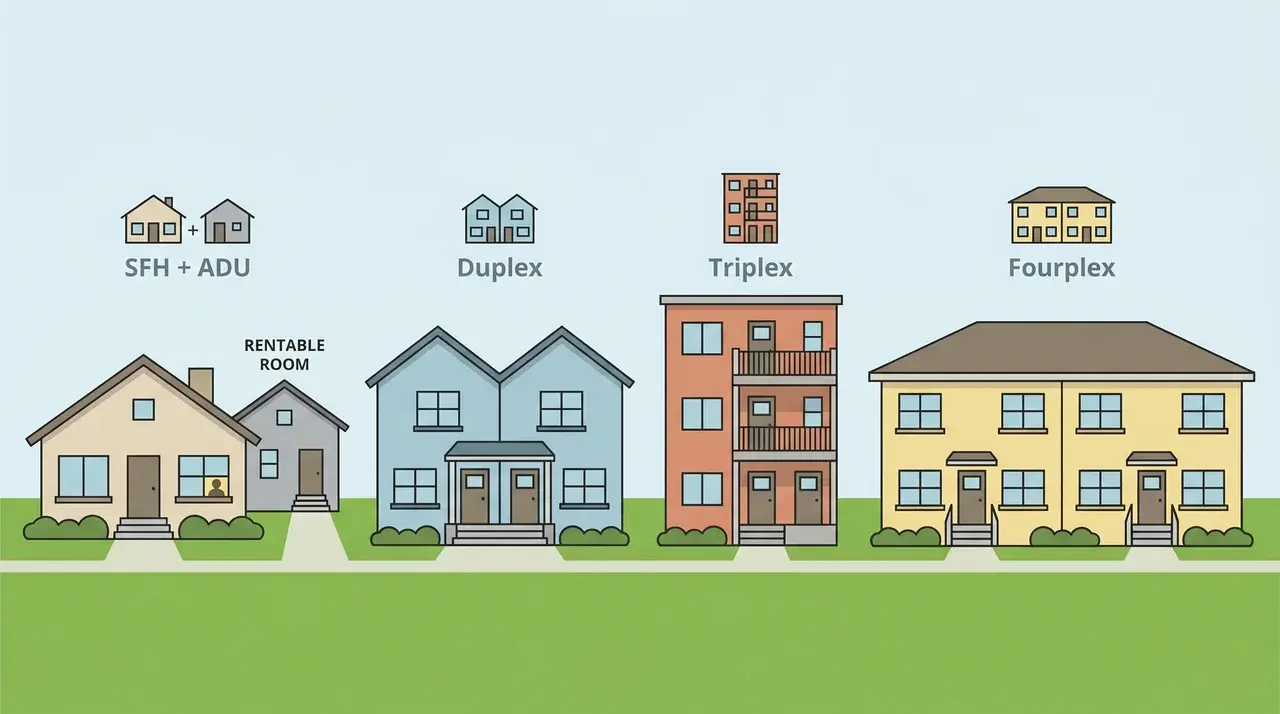

What Are the Common House Hacking Setups?

Two main property types work for house hacking. Your choice comes down to how much rental income you need and how much day-to-day contact you’re comfortable having with tenants.

Single-Family Setups

A single-family home works if part of the property generates rental income while you live in the rest. The most common setups are a spare bedroom, a finished basement unit, or an ADU on the same lot.

Short-term rentals through Airbnb or Vrbo fit here too. A spare room listed to travelers can earn more per night than a long-term lease, but the monthly income is less predictable.

The income ceiling on single-family setups is usually lower than multifamily. And if you’re planning to add an ADU or convert a garage, check local zoning first. Some cities restrict exactly what you can rent on a residential lot. Finding that out after you’ve bought is a painful lesson.

Small Multifamily Setups

A duplex, triplex, or fourplex is the setup most people picture. You live in one unit and rent the others. More units means more potential income and more physical distance from your tenants, which matters more than people expect.

You still qualify as an owner-occupant, so FHA and VA loans stay on the table.

The trade-off: larger properties cost more to buy and to run. When a unit sits empty, you feel it harder across a bigger budget.

I’d tell anyone considering multifamily to go in knowing it’s an active job, not a passive one. Better income numbers, yes. But you’re managing a small rental business from the unit next door.

Is House Hacking Worth It?

Housing is most people’s biggest monthly cost. Cutting it or wiping it out with rental income frees up real money. That cash can go toward savings, paying down debt, or other investments. That’s the real draw of house hacking, and it’s not overstated.

But the trade-offs deserve the same honest look. I’d rather you know them now than learn them after you’ve closed.

Privacy loss is the first one.

You share walls, common areas, or at minimum a property line with the people paying you. For some buyers, that’s fine. For others, it becomes a daily irritant within a few months. You know which type you are. Be honest about it before you buy.

Landlord responsibility is the second.

Screening tenants, enforcing leases, handling maintenance calls; these are yours now. Living on the property doesn’t lighten the load. If anything, it makes the friction feel closer.

The third constraint is local law.

Zoning rules and HOA restrictions can block short-term rentals, room leasing, or ADU builds in specific areas. A setup that looks great on paper can be off-limits where the property actually sits. Check this before you make an offer, not after.

House hacking trades lower housing costs for real responsibilities. For buyers who go in clear on that, it often works well. For buyers expecting it to run itself, it usually doesn’t.

The Bottom Line

House hacking isn’t complicated. You own a property, you live in it, and you rent part of it so tenants help cover your costs.

Whether it works comes down to the numbers in your specific market. What comparable rentals actually lease for, what vacancy looks like locally, what your real carrying costs are, those are the figures worth building your plan around, not rough estimates.

Start by looking at properties in your area and getting a real read on rental potential. The strategy is solid. Whether it fits your situation depends entirely on how honestly you run those numbers before you sign anything.

Frequently Asked Questions

What are the risks of house hacking?

The main risks are vacancy, landlord responsibility, and privacy loss. A vacant unit means you cover the full mortgage alone. You’re on the hook for maintenance, tenant screening, and lease enforcement. You also share your living space or at least your property with tenants. In some areas, zoning or HOA rules add another layer of constraint before you even get started.

What is an example of house hacking?

A common example: you buy a duplex using an FHA loan, move into one unit, and rent the other. The rent cuts your effective monthly cost. In a strong rental market, it can cover most or all of your mortgage payment, so you build equity while living there at a fraction of what ownership would normally cost.

How long do you have to live in a house to house hack?

Owner-occupant loan programs, including FHA and VA loans, require you to move in within a set window and treat the property as your primary residence. The exact occupancy term depends on the loan type and lender. The core rule is simple: you actually live there. Claiming it as a primary residence on paper while living elsewhere doesn’t count.

Is house hacking the same as having a roommate?

Renting a spare room is one version of house hacking, but the term covers much more; duplexes, ADUs, short-term rentals. The setup matters less than the underlying structure: you own the property, you live in it, and rental income reduces what ownership costs you each month.