When you wholesale real estate, you sell a contract, not a house. You find a distressed property, get it under contract at a discount, then hand that contract to a cash buyer for a fee. You never own the home. You never need a mortgage.

Most beginners think this takes serious capital or a real estate license. In most states, it takes neither. What you need is a signed purchase contract and a buyer ready to take it.

I’ll walk you through the process in exact order, from checking the law in your state to collecting your fee at closing.

What Is Real Estate Wholesaling?

Wholesaling means putting a distressed property under contract and selling that contract, not the property, to a cash buyer for a fee. The buyer pays the seller. You collect the gap between your contract price and what the buyer agreed to pay. That spread is your assignment fee.

Here’s what makes this legal: When you sign a purchase contract, you gain equitable interest. That’s the legal right to buy the property. You don’t own the house, but you own the right to buy it. That right is what you assign to the buyer. It’s the product you’re selling.

I’ve seen beginners trip over this every time. They think the deal is about the house. It isn’t. The deal is about the contract and one clause inside it.

Pull the “and/or assigns” phrase from the buyer field, and your right to assign disappears. You’d hold a contract with nothing sellable inside it.

Those three words are what create the asset. Without them, there’s nothing to transfer.

On the license question: in most states, assigning your own purchase contract doesn’t require a real estate license. But this varies by state. Some states treat wholesaling as brokering, which does require a license.

Before you sign your first contract, talk to a local real estate attorney. Getting this wrong doesn’t just kill a deal, it can mean fines or legal trouble.

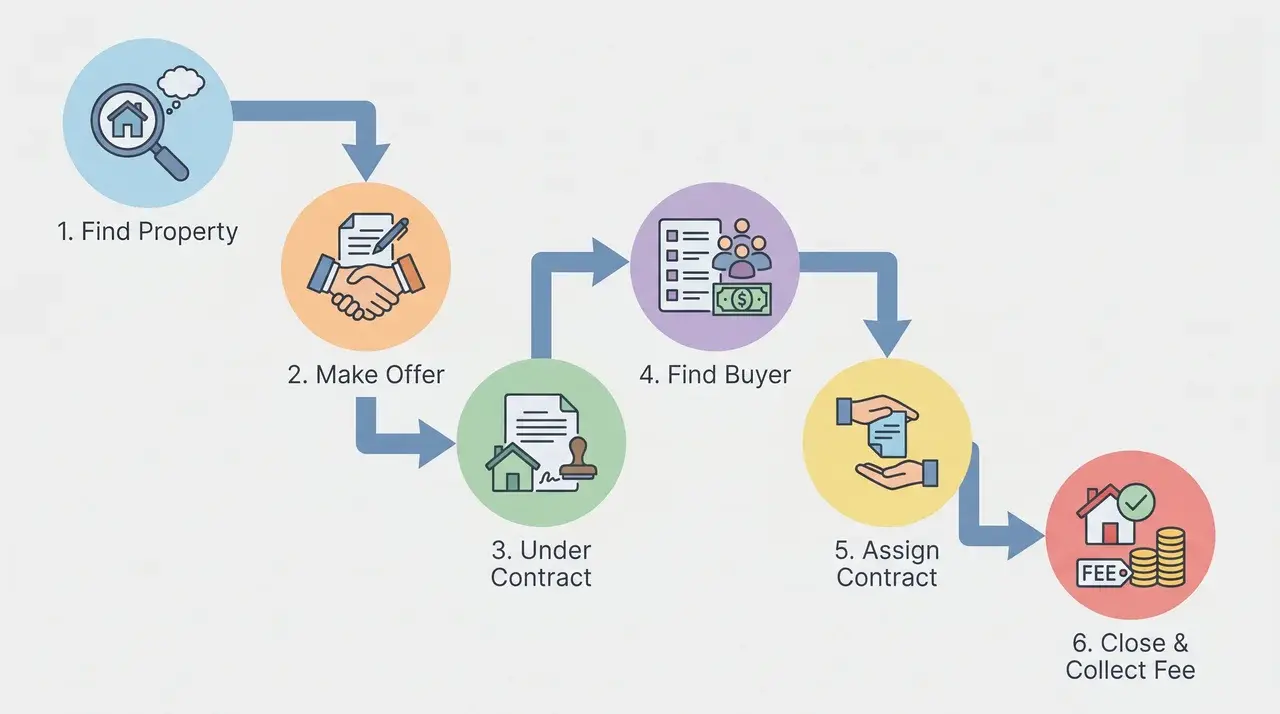

How to Wholesale Real Estate Step by Step

Every wholesale deal follows the same sequence. Skip a step or rush the order, and the deal falls apart, usually right before closing, when there’s no time left to fix it.

Step 1 — Research Local Real Estate Laws

This is the step most beginners skip because it feels like paperwork. Don’t skip it. Real estate laws vary by state and municipality. Some areas require a broker’s license or a wholesaler’s license before you can charge assignment fees.

Before you find a single property, talk to a local real estate attorney. Have them check your purchase contract and assignment agreement. That consultation costs far less than a deal falling apart at the title company over a legal problem you didn’t know existed.

Step 2 — Build Your Cash Buyers List First

The best wholesalers build their buyer list before they search for a single property. This is called reverse wholesaling. You already know what buyers want and what they’ll pay before you lock up a deal.

The two fastest ways to find cash buyers: attend local real estate investor meetups and search recent cash transactions in county records. Both are free.

When you’re under contract with a deadline ticking, five pre-built buyers who know your name beats a week of cold calls to strangers every time.

Step 3 — Find a Motivated Seller

You need sellers who want to move a property fast, not sellers chasing top dollar. The best leads come from people facing foreclosure, divorce, inherited homes they don’t want, or properties with serious deferred maintenance.

For sourcing, driving for dollars is the most accessible start. You physically note neglected, vacant, or fire-damaged homes in your target area. Pair it with direct mail to absentee owners, or pull pre-foreclosure lists from public records.

Tools like PropStream and BatchLeads automate off-market lead searches when you’re ready to scale.

Skip the MLS; listed properties almost never have enough margin for a wholesale deal to work.

Step 4 — Run the Numbers Using the 70% Rule

This is where most first deals die. Not in negotiation, but in the math done before negotiation even starts.

Cash buyers use the 70% Rule to set their ceiling. They won’t pay more than 70% of a property’s After-Repair Value (ARV), minus estimated repair costs. That number is called the Maximum Allowable Offer (MAO). Your contract price must sit below it. The buyer’s profit margin and your assignment fee both have to fit inside that gap.

Here’s how it works: if the ARV is $200,000 and repairs are $30,000, then ($200,000 × 0.70) − $30,000 = $110,000 MAO. Your contract price has to be below $110,000.

If the numbers don’t work on paper, they won’t work at the table. The buyer’s own comps will expose any inflated ARV the moment you present the deal.

Step 5 — Get the Seller Under Contract

When the numbers work, make your offer and get it in writing. Use a standard Purchase and Sale Agreement.

Before signing, check two things: “and/or assigns” must appear after your name in the buyer field, and the contract must clear your state’s assignability rules.

You’ll also need an earnest money deposit, typically around $1,000, paid to the title company. This is what makes the contract legally binding. It doesn’t go to the seller. It tells everyone involved you’re serious. Without it, the contract stands on shaky ground.

Step 6 — Assign the Contract and Close

Once a buyer agrees to take the deal, you sign an Assignment of Contract. This document transfers your purchase rights to the buyer for the agreed assignment fee. It names the original contract, both parties, the fee, and the closing date.

Your fee gets disclosed here. Cash buyers know it’s coming; they expect it.

I’ve seen wholesalers try to hide their fee, and it always backfires. Buyers talk to each other. Your reputation in a local market is what compounds your income over time, not any single deal. Be straight about the number.

At closing, the title company or escrow agent runs the transaction.

The end-buyer pays the seller the contracted price. Your assignment fee comes out of the buyer’s funds, not the seller’s proceeds. Stay reachable if the title company has questions. That’s it.

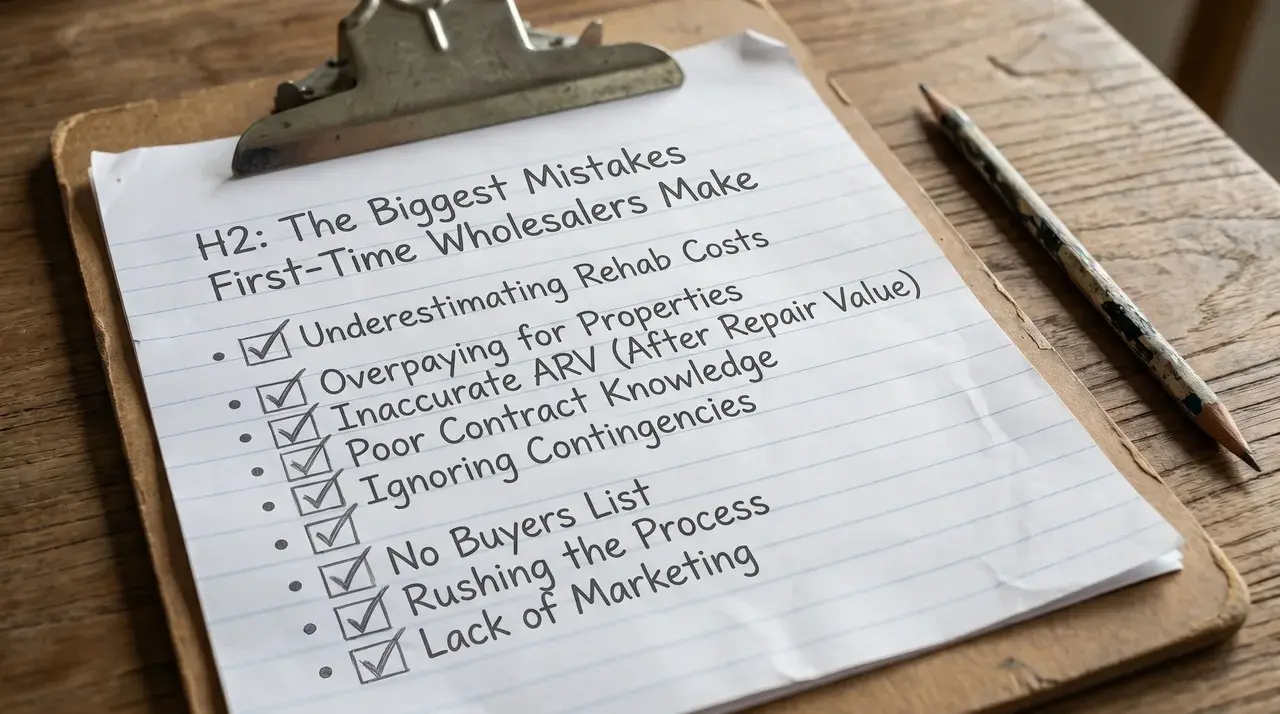

The Mistakes that Kill First Wholesale Deals

Most first deals don’t fail in negotiation. They fail because of fixable errors made before the seller is ever contacted. These four come up more than anything else.

Overestimating the ARV.

You run your numbers, get excited, lock up the contract, then present the deal to buyers. Their comps come back lower than yours. The deal dies, and so does your credibility with that buyer.

An inflated ARV doesn’t just kill this deal. It tells the buyer that your numbers can’t be trusted, which poisons every deal you bring them after. Pull your own sold comps from the MLS or through a title company contact. Never rely on an automated estimate.

Missing the “and/or assigns” clause.

Without that phrase in the buyer field, your contract isn’t transferable. You find out at the worst moment, when you have a ready buyer, and the title company flags the language.

Check every contract before you sign. This is a one-line fix that costs nothing to catch early and everything to catch late.

Building your buyer list after you find a deal.

You’re under contract with a clock running. You start cold-calling investors who don’t know you, pitching a deal to strangers.

I’ve watched deals expire exactly this way. Five pre-qualified buyers who return your calls is all it takes to avoid it. Build the list before you need it, not because you suddenly do.

Not checking assignability under local law before signing.

Some states restrict contract assignment or call it brokering. You won’t find out until the title company flags a compliance problem, by which point the earnest money is at risk, and the timeline is gone.

This is exactly why researching local laws matters. Legal review before the first contract is the fix. There’s no workaround once the clock is running.

Wrapping Up

The wholesalers who close deals consistently share one habit: they know their MAO before they ever call a seller. Get that number right, and the rest of the process has room to work. Get it wrong, and no negotiating skill saves the deal when the buyer runs their own numbers.

Legal compliance and a pre-built buyer list are what turn a first deal into a repeatable one. The wholesale real estate process runs the same way every time, but only cleanly when those two things are in place before the first contract is signed.

Frequently Asked Questions

How do I start wholesaling real estate with no money?

Wholesaling doesn’t require capital to buy property; your cost is time, not cash. You need a small earnest money deposit (typically around $1,000) to make your purchase contract legally binding, but you don’t fund the purchase. Your assignment fee is paid at closing from the buyer’s funds before you’ve spent a dollar on the deal itself.

Do I need a real estate license to wholesale?

In most states, no, but it depends on how you operate. Assigning your own purchase contract is generally legal without a license. Some states require a license if you’re marketing a property you don’t own or charging fees that look like broker commissions. Check your state’s laws and talk to a local real estate attorney before your first deal.

How much money can you make wholesaling real estate?

Assignment fees vary widely by market and deal quality. Most beginners close deals in the $5,000–$20,000 range per assignment. Larger markets and deeper buyer networks push that higher. The real variable isn’t fee size; it’s volume. Experienced wholesalers close multiple deals a month. Most first-timers spend months finding their first one.

What is the 70% rule in real estate wholesaling?

The 70% rule sets the most a cash buyer will pay: ARV multiplied by 0.70, minus estimated repair costs, equals the Maximum Allowable Offer (MAO). Your contract price must sit below the MAO. If it doesn’t, the buyer has no room for profit after repairs and holding costs, and they’ll pass.